My Place in the History of Computing - Part Two

What precipitated my move to the Big Time

At the beginning of 1980, I moved from the Hartford area to New York City. I was ready for another challenge. I had enjoyed my time in the investment department of CG (Connecticut General, the insurance company in Bloomfield, just outside of Hartford), but I felt I had reached the limits of my career opportunities there.

While at CG, I was developing skills and knowledge that would stand me in good stead in the Big City. I loved the challenge of using my computer skills to analyze complex investment problems. My favorites were those that involved some combination of tax law, regulatory requitements, actuarial projections, and probabilities of economic variables such as inflation and interest rates. I created models that would allow users to examine scenarios of their choosing so that they could get a feeling for the robustness of an investment.

In Part One of these reminiscences, I shared highlights from the early part of my career in computing and quantitative analysis. I ended this way:

As I sought more and more challenging problems to solve, my interests turned to finding a job that offered an opportunity to grow.

And grow I did! To mix metaphors: the meteoric rise in my career in the decade of the 1980s brought me fame and fortune in the world of international finance.

The PULL

In the earlier part of my career, I had been focused entirely on addressing challenges within the insurance company. Once I moved out of the data processing environment into the investment arena, my horizons widened.

Part of my job involved evaluating software that could aid our investment professionals. To that end, I was dispatched to attend sales pitches at venues such as The Lodge at Pebble Beach. (I was never a golfer, but I did enjoy getting out at dawn onto the course to run a few miles along the fairways, before the golfers arrived. The grazing mule deer would look up at me as some kind of an oddball who didn’t know how to use a golfcart.}

My boss, Bob Whalen, was connected with a wider community of quantitative financial analysts, and he arranged CG to be a member of the “Q Group” (then affiliated with Columbia University). The membership entitled two people to attend meetings, so Bob brought me along, and I got to meet many fellow “quants” (an affectionate — or derisive, to some outsiders — term used to describe those of us who used computers to analyze investment problems). In those days (the late 1970s), there were probably about 100 quants in the country, and I got to know them all.

I also had earlier met many of the Q Group members who worked on Wall Street because they came to our offices in Connecticut to pitch their wares. More on those people in a future post, when I discuss my creation of QWAFAFEW at greater length.

One such person was Tony Estep, later to become a good friend and one of the founding members of QWAFAFEW. When I was at CG, he was working for a large Wall Street brokerage firm, and he came to sell us on the use of his DDM (Dividend Discount Model). While his explanations of the model probably mostly went over the heads of the CG portfolio managers, I immediately grasped the concepts he was detailing. I remember thinking, “I could do that!”

At around that time, my friend Brooke told me that he had found an opportunity in the City that would mean he was moving away. I was sorry to learn of his departure, but I was excited to learn of his new job. He would be getting in on the ground floor of a rapidly expanding software business, and his salary would be twice what he was earning at CG. All of that certainly caught my attention.

Through my Q Group contacts, I began to put out the word that I was looking for a chance to make a similar move.

In addition to the pull of the bright lights of the big city, there were push factors urging me to seek a fresh start.

The PUSH

On the personal side, I had recently gone through my second painful divorce. I had some rebound romances that were fun while they lasted, but I was feeling a need for a change in scenery.

In my professional life, one of my joys was developing new products. Later in this post I will describe my CAM (Customized Asset Mix) Model, as well as a preview of later work. CAM represented to me the pinnacle of the work I had done at CG.

Once CAM was up and running, I came up with (what I thought was) a brilliant idea for an even more sophisticated product. After my proposal had been rejected by upper management, I realized that I needed to be in an environment that was more welcoming of creativity.

The new product I had proposed was a fixed-income strategy that would provide a long-term guaranteed rate of return with no risk to the insurance company. My boss thought it was a promising idea, and I had an ally in the fixed-income department.

When I entered the Masters degree program in Economics at Trinity College in 1972, Professor Tom Steffanci administered the entrance exam. Since I had just received my BA in Economics, I did not bother to bone up on the subject matter. Much to my chagrin, the test focused on details that I had studied many years earlier. Since I was a part-time student, it took me nine years to complete my BA, and Economics 101 was a distant memory. I failed the exam, meaning that I would be required to retake the basic courses before I could be admitted to the Masters program.

I scheduled an appointment with Professor Steffanci to protest, and to explain my situation. “All right,” he agreed, “you can start at the graduate level. I will be giving a quiz in the third week of class, and if you fail that you will have to drop out and take the remedial courses.” With that hanging over my head, I studied the course material as if my life depended on it.

I was usually on time for the weekly classes, but for the session following the quiz, a crisis at work resulted in my being a few minutes late. “Ah, Mr. Wilcox,” the professor said as I walked in and sat in the back of the room. “I was just giving out the grades from the quiz, and I mentioned your name.” Uh-oh! I thought, fearing bad news. “Yes,” he continued, “you received a perfect score on the exam, the highest mark I have ever given.” Ah, what a relief! Not long after that, Tom and I became good friends.

And then, several years later, after I had been in CG’s Investment Department for a couple of years, Tom was hired as a fixed income portfolio manager. I was surprised and delighted to have him join the team. Bond management is, by its nature, more quantitative than equity management.

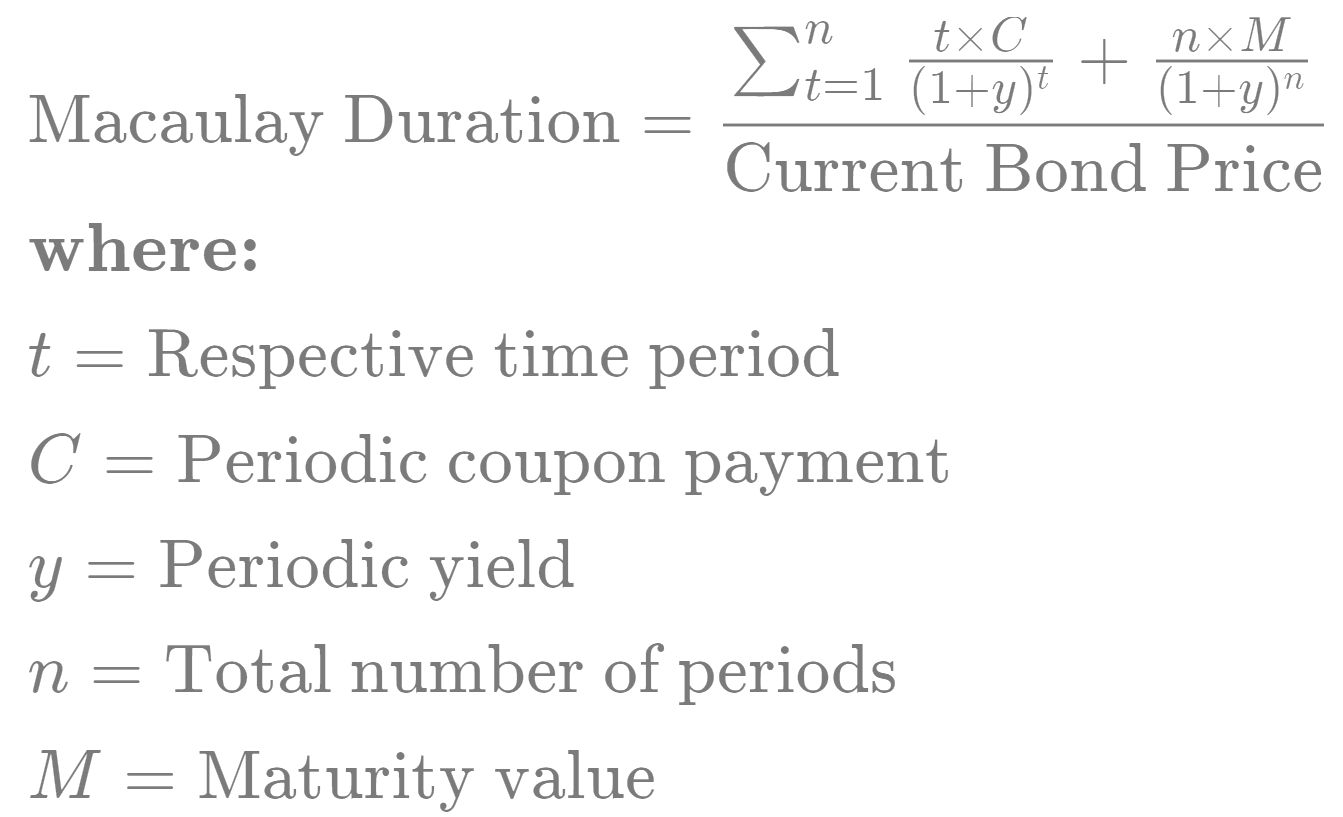

By that time, I was well versed in the mathematics of bond management, and I had come up with the scheme for a guaranteed rate of return. My idea was based on a fairly simple concept that had been developed by Frederick Macaulay in the 1930s — that of bond duration. While the concept [the present-value weighted average time to payment of the cash flows from a bond] is fairly straightforward, solving for the expected rate of return (y in this example) is not.

Macaulay published many tables of relevant statistics, using various assumptions. In his day (and up to the time of the Apollo program) a “computer” was a person, not a machine. Using pencil and paper and an aptitude for mathematics, computers (who were usually women, based on the accounts I have read) would calculate the values to fill in tables of duration and a host of other computations, such as for logarithms.

In the 1970s, I had access to APL and digital (machine) computers, and the calculations became trivial. I developed and documented a duration-matching strategy to deliver those guaranteed returns with no risk to the guarantor.

I went to Tom for advice on how to present the idea to our management team. Tom wanted to be the one to propose it. He set to work on describing the process and making the case for why it would be appealing to potential investors.

Our idea was shot down — the reason given was that the company had decided to stick to its knitting. They were making good money offering to manage plain vanilla stock, bond, and asset mix portfolios, and felt no need for a fancy new product.

Tom and I were both very discouraged by this attitude, and within a short time both of us left for greener pastures. Ironically, I ran into Bob Whalen at a conference a few years later, and he told me he had finally convinced his superiors of the value of my idea. By then, the strategy had been adopted by other asset management firms, and went by the acronym GIC (Guaranteed Interest Contract). Bob told me that CG now managed billions of dollars that way, and was the largest GIC provider in the world.

CAM

The technology behind the Customized Asset Mix (CAM) model included the latest, most sophisticated software and hardware systems. The entire model was written (by me) in APL, and the output included graphs drawn on an HP plotter. Later models of HP plotters featured several pens of different colors, but in the beginning the plotter had a single black-ink pen, and could produce hard-copy graphics like this one:

I thoroughly documented each subroutine in the model.

I also wrote several memoranda documenting the reasoning behind the modeling. One of my key discoveries, in doing research for the process, was Gibrat's law of proportionate effect, as defined by Robert Gibrat (1904–1980) in 1931. Although not referenced directly in the references shown below, it was described in the Steindl paper. In essence, the Law stated that a random growth process (something widely observed both in nature an in human activity) will be proportionate to size, and will result in a size distribution that is lognormal. This could apply to the size of cities, for example, or to the value of a firm (or any other investment where single-period returns are random).

Brownian motion, cited by Einstein in a couple of his (circa 1905) papers as evidence of the existence of atoms, was thought by some to represent investment returns in the stock market. There was some disagreement, however, among academics (and practitioners) as to whether longer-term returns would be distributed normally (in a bell-shaped function) or lognormally (the logarithms of the results form a bell-shaped curve). I made what I thought was a convincing argument for lognormality.

At my request, my Actuary friend and colleague Dick Murphy produced a multi-page (hand-written) derivation giving a formula for computing the value of any section of a lognormal distribution. I used that in creating the graphics you see illustrated here.

One of the goals of the CAM model was to show small business owners how they would benefit from gradually moving money out of CG’s General Account into Separate Accounts that offered better long-term return expectations. This could not be done all at once because of insurance regulations, so the model was build to take into account those constraints.

A Hint at what Will Be in Part Three

In Part Three of this brief description of my career, I will have more to say about what I did in the decade of the 1980s, after I left Connecticut.

There will not be a quiz on what follows here. The document reproduced below was produced after my time on Wall Street.

I had moved to Boston in 1991 to work for a large bank there. It was a move from the sell side (brokerage) back to the buy side (money management). I managed billions of dollars of international assets for clients, and created custom-made products to meet their needs. From there, I left to establish my own consulting and research business, and did a lot of expert witness work. In order to help promote my business and meet prospective clients, I spoke at many investment conferences all around the world. This is a sample handout from one of my talks.

I appreciate your career history and thank you for the courage to share.